Select a version to view

Neural Network Stock Trading System

A learning-focused machine learning project built entirely from scratch — demonstrating my ability to design, optimize, and evaluate neural networks without relying on pre-built ML frameworks.

Project Overview

This project is a self-built neural network trading system that analyzes minute‑level stock data and attempts to generate buy/sell decisions. The focus of this project was not to build a profitable trading bot, but to fully understand how neural networks work at the lowest level — from matrix operations to training logic.

Why this project matters:

- I implemented a complete neural network using only NumPy — no TensorFlow, PyTorch, or ML libraries.

- I created a custom learning and evaluation strategy to optimize the model.

- I simulated trading decisions and evaluated them with a performance metric I designed myself.

- The project shows my ability to work independently, build complex systems, and quickly learn advanced ML concepts.

How the System Works

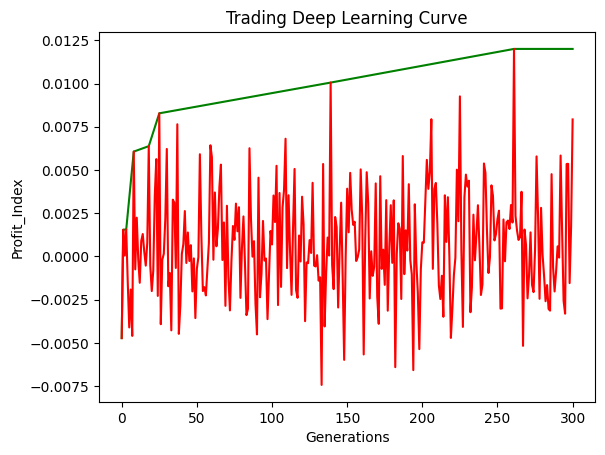

The model takes short windows of historical TSLA price data and outputs a probability for buying or selling. Instead of classical backpropagation, I used a simple evolutionary strategy, repeatedly adjusting the model’s weights and keeping the best-performing version.

Key Components

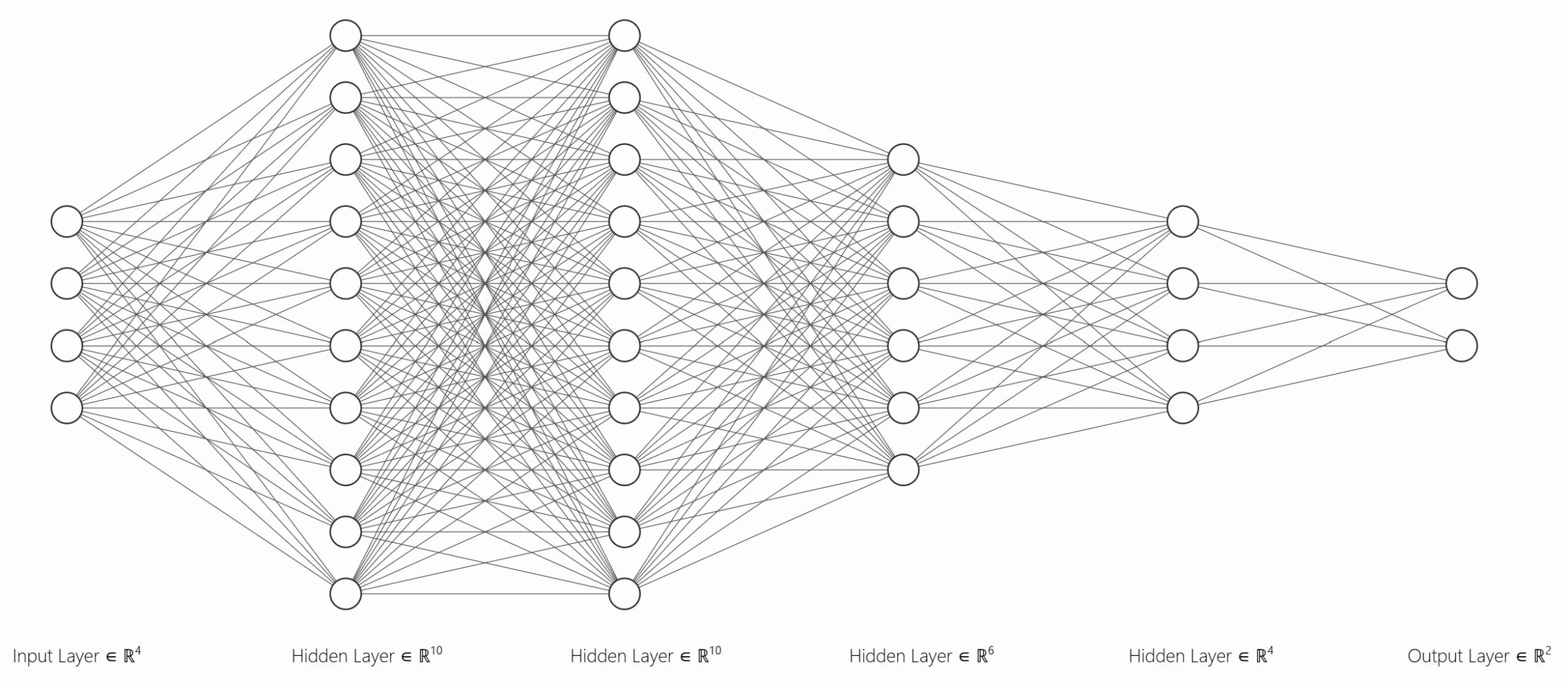

- Custom Neural Network: Several fully connected layers coded manually.

- Evolutionary Training: Small informed changes to the model, keeping better-performing generations.

- Profit Index: My own scoring function to judge trading performance.

Architecture

Illustration of the multi-layer network used (simplified for visualization).

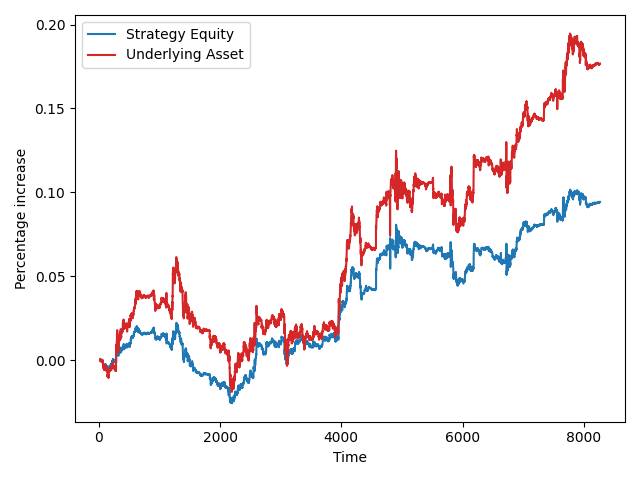

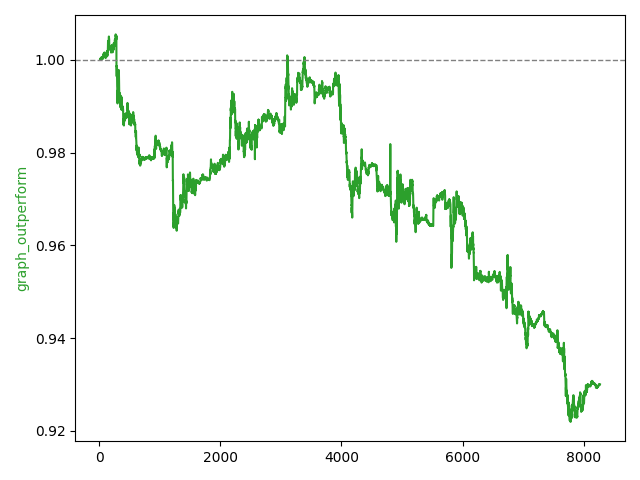

Simulation & Testing

I ran the model across historical 1‑minute TSLA data, simulating buy/sell decisions. The Profit Index rewarded:

- Correct direction predictions

- High-confidence decisions

- Stable, repeatable performance over many data slices

Results

While the system did not produce a profitable trading strategy, it successfully demonstrated that:

- I can independently design and implement a multi-layer neural network.

- I understand how data preprocessing, weight initialization, activation functions, and output interpretation work under the hood.

- I can build custom evaluation metrics and training loops without relying on existing tools.

What I Learned

This project provided deep, practical intuition about modern machine learning. Key learnings include:

- How neural networks behave internally (beyond high-level libraries)

- How to structurally debug ML models and interpret unstable learning behavior

- The challenges of financial time‑series prediction

- How to design experiments, evaluate performance, and iterate methodically